ATLANTA, GEORGIA – May 30, 2017 – Georgians routinely enter into contracts for everything from cell phone service to apartment leases, even employment, but many sign contracts without fully understanding that their signature potentially forfeits their fundamental rights. By signing a contract that includes a mandatory arbitration clause, consumers waive their rights to sue in court, to participate in class action lawsuits, or to appeal. Arbitration clauses often hide in contracts’ fine print and require the parties to forfeit the right to go to court to resolve any dispute. Arbitration is a form of alternative dispute resolution that takes place outside of the judicial system and renders binding decisions that often favor businesses, not consumers. If the arbitration process gets it wrong, there is no recourse for a harmed consumer.

{kind=link}

Last year, banking giant Wells Fargo was fined $185 million dollars for fraudulently opening millions of fake accounts and credit cards in the names of account holders without their knowledge or consent in an effort to meet aggressive sales quotas. Many of the consumers incurred fees from the bogus accounts and had their credit scores ruined, but the bank has been able to keep consumers from pursuing legal action because the contracts they signed to open their legitimate accounts mandated private arbitration with the bank.

What is being done to help ensure that consumers have access to civil justice when they are harmed by bad business practices?

Congressional Action

To address this critical issue, Georgia Congressman Hank Johnson (D) has convened a coalition of seven senators and congressmen to highlight the importance of access to justice in courts for consumers, workers and small businesses. Among his efforts, Rep. Johnson has co-sponsored the comprehensive Arbitration Fairness Act of 2017, proposed legislation to amend the Federal Arbitration Act to eliminate forced arbitration clauses in employment, consumer, civil rights and antitrust cases. The legislation is designed to protect consumers and workers and hold corporations accountable for wrongdoing.

According to the Arbitration Fairness Act, arbitration frequently lacks the procedural processes that allow plaintiffs to prove their case, does not allow for judicial review, lacks meaningful transparency, impairs the development of important federal laws, and is plagued by “repeat-player bias,” biasing arbitrators hired by companies to decide in their favor in order to generate repeat business. Mandatory arbitration clauses advantage businesses and strip consumers of their right to go to court and render them essentially powerless in disputes with businesses.

The Federal Arbitration Act was enacted in 1925 to target commercial arbitration agreements between companies of generally comparable bargaining power. Over the years, however, the U.S. Supreme Court in its rulings have broadened the power of the FAA, which was not intended to cover consumer disputes. Because of the Court’s deference to the FAA, lower courts are forced to honor arbitration clauses, even when they foreclose the opportunity to vindicate consumer rights that are guaranteed by state or federal law.

Rep. Johnson’s Arbitration Fairness Act is intended to restore the original intent of the FAA by clarifying the scope of its application. Arbitration can be a viable alternative to litigation if entered into voluntarily and after a dispute arises, but the current application of the FAA allows corporations to insulate themselves from liability by forcing consumers to preemptively give up their rights. The proposed legislation would amend the FAA to invalidate agreements that require arbitration of disputes before the dispute arises. The Act would not ban arbitration or restrict use when both parties agree. It would provide for the opportunity to enter into arbitration agreement after a dispute has arisen, affording consumers a meaningful choice about how to proceed with their claim.

CFPB Proposed Rules

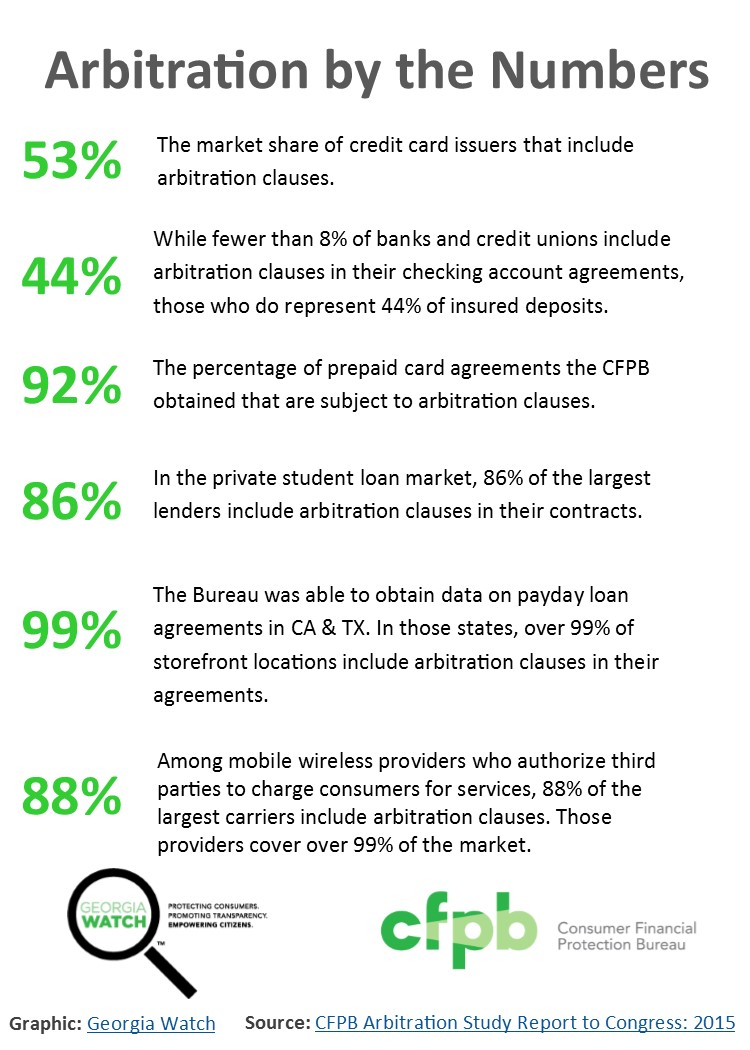

The Consumer Financial Protection Bureau (CFPB), a federal agency that advocates for the protection of consumers in the financial marketplace, is also focusing on this crucial issue. The CFPB is developing rules to protect consumers from fine print that affects hundreds of millions of contracts for credit cards, payday loans, student loans, bank accounts and many other financial services. The agency is proposing three benefits to consumers: access to court, deterrence for companies and increased transparency.

Court Access: A CFPB study found that many consumers do not realize when their rights are violated and often the harm is too small nominally to make it practical for a single consumer to pursue an individual dispute. The study found that only two percent of consumers would bother to consult an attorney or pursue legal action over small dollar disputes. The CFPB has proposed a rule that would prohibit banks and lenders from using mandatory arbitration clauses that block class actions, so consumers would be free to either file a class action or to join one. Under the proposal, companies would still be free to use arbitration clauses, but the clauses would have to clearly state that they cannot be used to prohibit consumers from being part of a class action case in court.

Deterrence: The proposed rules would incentivize companies to comply with laws to avoid group lawsuits since, when companies are held accountable, they are less likely to engage in unlawful practices that can harm consumers. Also, public attention on the practices of one company in an industry can influence and affect not only that company’s business practices, but also business practices of others within the industry.

Transparency: The proposed rules would also require that companies submit to CFPB any claims, awards and certain materials related to arbitration cases so that the agency could provide oversight to ensure that the arbitration process is fair to consumers. CFPB would also collect correspondence from arbitration administrators to ensure compliance with arbitration standards of conduct. Collecting these materials helps CFPB better understand and monitor arbitrations to promote fairness in the process.

Georgia Watch supports CFPB’s proposed rules because they would increase transparency and understanding of the impact of mandatory arbitration, restore access to judicial remedy for millions of consumers, and provide for agency oversight and reporting of critical data related to these disputes.